• reduce the emissions they control directly to net zero by 2040, with an ambition to reach an 80% reduction by 2028 to 2032

• reduce the emissions they can influence to net zero by 2045, with an ambition to reach an 80% reduction by 2036 to 2039

Skip to main content

The briefing sets out the NHS environmental sustainability commitments and reporting requirements across the United Kingdom, what NHS organisations must report in 2023/24, along with good practice in sustainability reporting for NHS organisations in 2023/24 and beyond.

It also looks ahead at future developments, the role of the finance function and how you can get involved in supporting the agenda.

There is no doubt environmental sustainability is a key challenge for everyone. The Conference of Parties (COP) 28 included its first ever health day with a declaration on climate and health

Amanda Pritchard, NHS England chief executive

Each of the four nations of the UK has net zero targets; sustainability reporting is therefore a key mechanism to manage progress towards achieving them. In the private sector, sustainability reporting is increasingly important to investors and stock exchanges, while in both the private sector and public sector it is important to support decision-making and accountability.

As a result, sustainability reporting is an area of increased focus across the accountancy profession and is expected to increase in prominence over the coming years.

The current sustainability reporting landscape is complicated, with different government departments responsible for different policies. Sustainability reporting requirements, and the planned timing of implementation, varies across the private sector and public sector, as well as across different parts of the public sector itself.

2023/24 is the first year that public sector bodies will be required to include some of the task force on climate-related financial disclosures (TCFD) in their annual reports. This is the first of three phases that will result in TCFD compliance, as adapted for the public sector, by 2025/26.

The role of the finance function in driving effective sustainability reporting is critical, not only in meeting mandatory requirements but leading the way in driving sustainability reporting and sharing best practice.

The aim of this briefing is to signpost finance directors, sustainability leads, non-executive directors and all those interested in the environmental sustainability agenda to guidance and reporting requirements that are, or may become, relevant to the NHS.

The briefing sets out the NHS environmental sustainability commitments and reporting requirements across the United Kingdom, what NHS organisations must report in 2023/24, along with good practice in sustainability reporting for NHS organisations in 2023/24 and beyond. It also looks ahead at future developments, the role of the finance function and how you can get involved in supporting the agenda.

There is a clear commitment to improving environmental sustainability in the NHS across the United Kingdom, as set out in legislation, strategies and guidance. As shown in figure 1, each of the four nations has ambitious targets to reduce carbon emissions.

Figure 1: NHS carbon emissions targets

In October 2020, the NHS in England became the world’s first health service to commit to reaching carbon net zero. Along with targets set out in Delivering a net zero national health service, environmental sustainability requirements in England are reflected in the following:

The Climate Change (Scotland) Act 2009

NHS Scotland’s policy aims are to ensure that it:

contributes to the achievement of the United Nation’s Sustainable development goals

To underpin these policy aims, the Scottish government has included climate and environment as delivery priorities in the NHS Scotland delivery plan guidance 2024/25

The Climate Change Act (Northern Ireland) 2022

In addition to and predating the Climate Change Act, Northern Ireland also has an Energy management strategy and action plan to 2030

The Welsh Government declared a climate emergency in 2019 and has set the ambition for the public sector in Wales to be net zero by 2030. In March 2019 the First Minister for Wales launched Prosperity for all: a low carbon Wales

The NHS Wales decarbonisation strategic delivery plan

The Well-being of Future Generations (Wales) Act 2015

To support effective sustainability decision-making and accountability, information is needed to measure progress against targets. Sustainability reporting allows organisations to understand their current position and compare themselves to targets, both over time and with other organisations.

As CIMA observed

Sustainability reporting for the future

There is a range of guidance applicable to different organisations and at different times as set out below. The 2024 HFMA pre-accounts planning conference session on environmental reporting requirements for NHS bodies

Companies and limited liability partnership regulations include requirements that strengthen environmental, social and governance (ESG) reporting. They require disclosure, where material, of how climate change is addressed in corporate governance; the impacts on strategy; how climate-related risks and opportunities are managed; and the performance measures and targets applied.

The regulation’s requirements are aligned with the recommendations issued by the TCFD

These requirements, as adapted for the public sector, will be applied from 2023/24 (see further detail in the NHS 2023/24 reporting requirements section below).

The GRI standards are a modular system of interconnected standards to help organisations report the impacts of their activities towards sustainable development. They are designed to enable any organisation to understand and report on their impacts across the economy, environment, and people in a comparable and credible way to increase transparency on their contribution to sustainable development.

Although the use of GRI is not an NHS requirement, there are ambitions to develop sector-specific measures for healthcare

IFRS S1 General requirements for disclosure of sustainability-related financial information

The UK government has established the UK Sustainability Disclosure Technical Advisory Committee

Neither IFRS S1 nor IFRS S2 have yet been endorsed by the secretary of state for use by UK companies, so are not yet mandated for use.

Following consultation in 2022, the International Public Sector Accounting Standards Board (IPSASB) is also considering plans to develop a public sector specific sustainability reporting

HM Treasury and the Financial Reporting Advisory Board (FRAB) are monitoring developments by standard setters, as well as in the private sector, to consider and advise on a future sustainability-related reporting strategy for the UK public sector.

The Greening government commitments (GGC) framework includes targets on greenhouse gas emissions, waste and water consumption, as well as commitments on procurement, nature recovery, climate adaptation and information and communication technology.

They are applicable to central government departments and their agencies. NHS bodies are excluded from the scope of these.

The 2024/25 FReM refers to mandatory sustainability reporting requirements including the impact of the entity’s business on the environment and reporting on climate change adaptation. It also refers to the Sustainability and environmental reporting guidance

The FReM does inform the contents of the various accounting manuals that NHS bodies across the UK are required to comply with, and so informs the contents of the manuals for all four nations. These are set out further below.

The main changes to the 2023/24 FReM are focussed around the sustainability reporting in relation to the TCFD aligned disclosure application guidance. Phase one is a high level overview of the governance of an organisation, and the recommendation within the governance pillar of the TCFD framework is that the accounts include disclosure of the organisation’s governance around climate change related risks, and opportunities. Recommended disclosures are that the board’s oversight of climate-related risks and opportunities is described, along with management’s role in assessing and managing climate-related risks and opportunities. Where data is already available, metrics and targets can be specified. This Treasury guidance describes best practice, so is equally valid across the four nations of the United Kingdom.

The TCFD guidance itself does not automatically apply to local government, NHS bodies (trusts, foundation trusts and integrated care boards), or entities in devolved administrations. However, relevant authorities, such as the DHSC may direct entities to follow the guidance, as set out or in an adapted form, and it is considered best practice.

The guidance will be implemented in phases, with phase one applying to English accounts from 2023/24, with the other nations and phases to follow.

NHS bodies that have more than 500 full-time equivalent employees or have total operating income of more than £500m will be required to comply with the first of three phases of TCFD in 2023/24.

The new disclosure requirements will be incorporated into the 2023/24 GAM

Confirmation of the changes incorporated into the GAM covering 2023/24 will be included as part of the April 2024 additional guidance

As previously required, progress against targets set out in each NHS body’s green plan

Preparers may also cross-refer to disclosures elsewhere in the annual report such as the annual governance statement or other content such as green plans rather than duplicate this material in this section of the annual report.

This allows for significant flexibility by NHS bodies in terms of the level of detail they report.

The NHS standard contract also stipulates (service condition 18.2) that providers must maintain and deliver a green plan, approved by their governing body, in accordance with guidance and must:

Green plan requirements for trusts and integrated care systems are provided by Greener NHS.

As reflected in model annual governance statements 2023/24

NHS health boards are required to prepare their accounts in accordance with the Scottish public finance manual

The Climate Change (Duties of Public Bodies: Reporting Requirements) (Scotland) Amendment Order 2020

In addition, health boards are required to report on their progress against NHS Scotland’s climate and sustainability aims on an annual basis under A policy for NHS Scotland on the climate emergency and sustainable development

Audit Scotland is developing a programme of work on climate change. For 2023/24 audits

The 2023/24 Government financial reporting manual

The format and presentation of statutory accounts are prescribed by NHS Wales and are based on the guidance in the FReM. In accordance with the FReM, Welsh health bodies publish sustainability information within their annual report, comprising high-level overviews of the impact of the entity’s business on the environment and their work on environmental matters.

In addition, and outside of annual reporting, Welsh public sector bodies including health bodies must report their well-being and sustainable development plans and progress to the auditor general. The auditor general undertakes examinations

Sustainable development plans must also be shared with the future generations commissioner and NHS Wales’ planning framework

Good practice sustainability reporting should provide the information the reader needs, such as clear and timely information they need to understand the position on environmental sustainability and drive improved actions.

There are a number of good practice examples of sustainability reporting with some NHS bodies trialling approaches from a simple table of requirements and progress against the standard contract, to the mapping of carbon impact against individual lines in their ledger.

Examples of sustainability reporting are set out below for reference. While the information listed in these examples is neither exhaustive nor mandatory, it may be a useful guide for preparers of annual reports of the types and broad headings of information that readers will find useful.

NHS England

Newcastle upon Tyne Hospitals NHS Foundation Trust was the first healthcare organisation in the world to declare a climate emergency. Their 2022/23 annual report

Manchester University NHS Foundation Trust, provides readers with information on its carbon footprint plus the emissions over which they have influence in its 2022/23 annual report

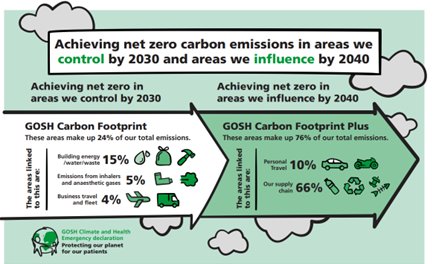

As shown in figure 2, Great Ormond Street Hospital NHS Foundation Trust , cited as best practice by the National Audit Office (NAO) in Good practice in annual reporting

Figure 2: Great Ormond Street Hospital NHS Foundation Trust annual report 2022/23 extract

Welsh health boards publish high-level summary sustainability information in their annual reports with reference to more detailed reporting.

Velindre University NHS Trust’s annual report

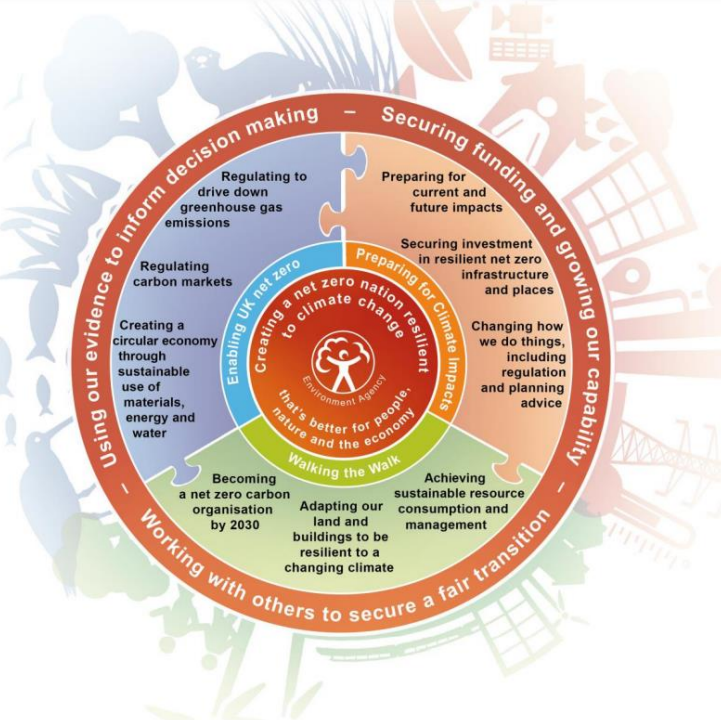

HM Treasury has published a review of examples of best practice in annual accounts

Figure 3: Environment Agency climate ambition in HM Treasury’s Best practice examples 2021/22

The NAO Good practice in annual reporting highlights annual reports from a range of organisations for their consideration of the environment in which the entity operates, stakeholder engagement and integration of sustainability into core strategy.

From the global corporate reporting sector, Olam group’s annual report

The role of the finance function in driving effective sustainability reporting is critical. This role extends beyond meeting the requirements set out for inclusion in the annual report and accounts. With a number of question marks over metrics, evolving guidance and often pockets of reporting in silos, the finance function has the necessary skills to analyse and report measures, and to bring together different sources of information and people. Crucially, the finance function can identify, and provide early warning of, operational and risk drivers linked to sustainability efforts, and their potential impact on the overall financial position.

CIPFA notes

ACCA’s Green budgeting toolkit

The finance function also has a role in ensuring climate change risks are on the board agenda, considered as part of the overall strategy and proactively in decision-making. The Care Quality Commission (CQC) well-led quality statements

The impact of climate-related risks is also an area of increasing audit focus as a result of the Financial Reporting Council's (FRC) review of TCFD disclosures

The NAO guide, Climate change risk: a good practice guide for audit and risk assurance committees

Audit committees in particular should be aware of the planning and reporting requirements and be able to offer sufficient challenge and assurance to help organisations implement their plans (including milestones and metrics) and hold the board and individuals to account.

There are a number of training programmes and guidance available, such as ICAEW and CIPFA's Public sector sustainability certificate

We will continue to update our briefing as requirements and standards develop. Please get in touch via [email protected] if you would like to share your own examples from 2023/24 or would like to get involved in supporting this agenda.

The Institute’s annual costing conference provides the NHS with the latest developments and guidance in NHS costing.

The Estates and Facilities forum is designed to enable finance leaders and senior facilities staff to explore how capital can be financed